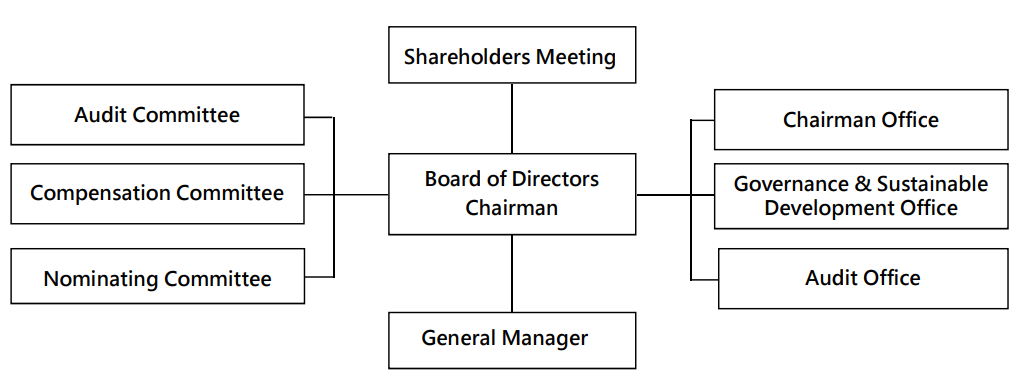

- Board of Directors

- Committees

- Governance & Sustainable Development Office

- Internal Policies

- The operational status of Corporate Governance

- Implementation status of performing Ethical Corporate Management

- Prevent Insider Trading

- Internal Audit

- Risk Management

- Whistle Blowing System

Purpose of Internal Audit

The internal control systems of the company are management processes followed by the Regulations Governing Establishment of Internal Control Systems by Public Companies, passed by its board of directors, and implemented by the board of directors, managers, and other employees for purpose of promoting sound operations of the company, so as to reasonably ensure that the following objectives are achieved:

1. Effectiveness and efficiency of operations.

2. Reliability, timeliness, transparency, and regulatory compliance of reporting.

3. Compliance with applicable laws, regulations, and bylaws.

Internal audits aim to assist the board of directors and mangers in inspecting and reviewing defects in the internal control systems as well as measuring operational effectiveness and efficiency, and shall make timely recommendations for improvements to ensure the sustained operating effectiveness of the systems and to provide a basis for review and correction.

Structure of Audit Office

The audit office of the company is subordinate to the board of directors, and is equipped with full-time internal auditors. The qualifications meet the requirements of the Regulations Governing Establishment of Internal Control Systems by Public Companies. Any appointment or dismissal of chief internal auditor of the company shall be subject to approval by the board of directors. The company shall report to the FSC for recordation the names, ages, educational background, experience, seniority, and training of its internal auditors by the end of January each year via the Internet-based information system.